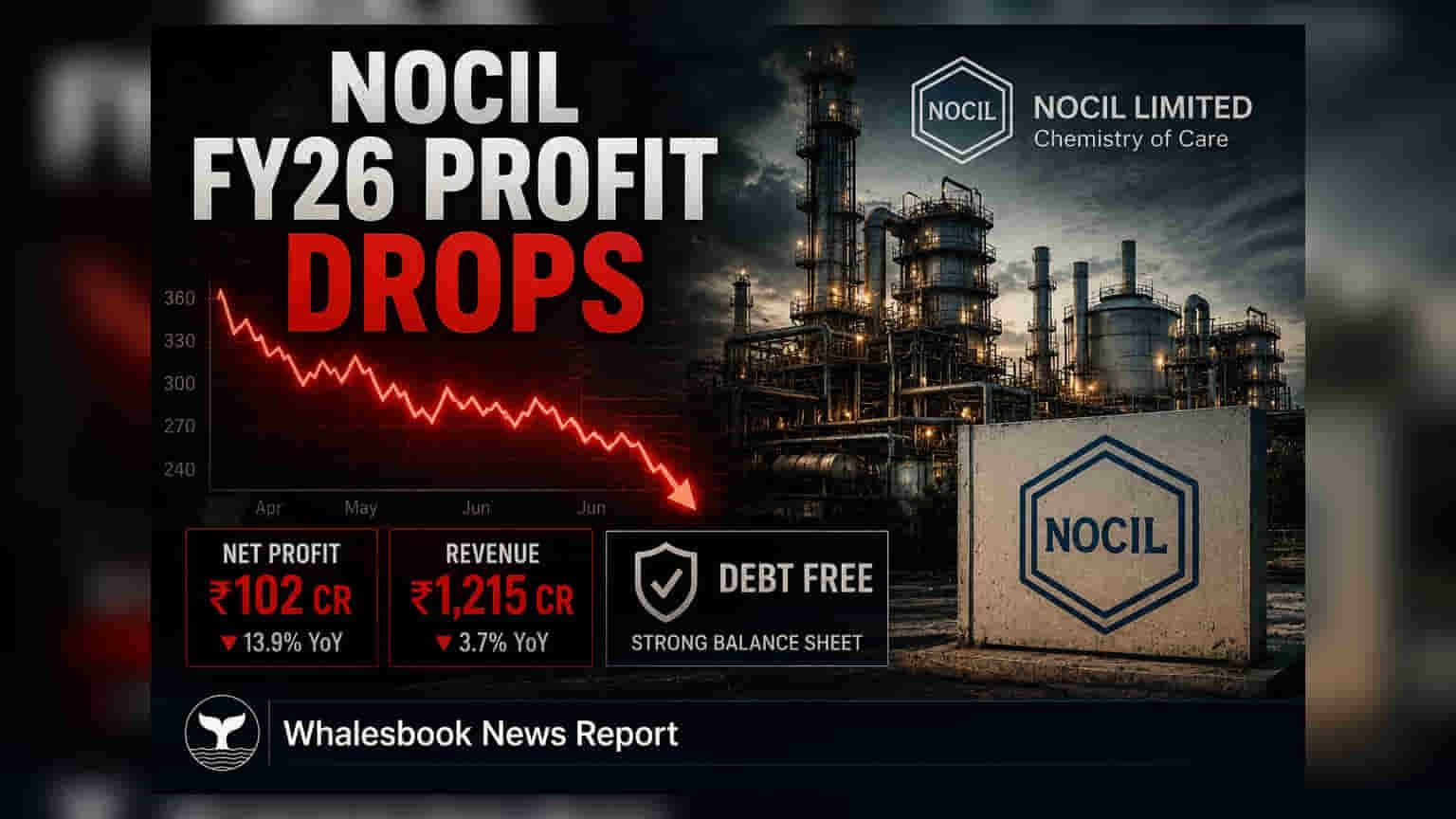

NOCIL's FY26 revenue fell 6.44% to ₹1,302.97 crore and net profit dropped 40.42% to ₹64.09 crore due to pricing pressures. The company recommended a final dividend of ₹1.50 per share.

NOCIL Reports FY26 Revenue Dip Amid Global Competition

NOCIL's revenue from operations for the fiscal year ended March 31, 2026, stood at ₹1,302.97 crore, a decrease of 6.44% from ₹1,392.69 crore in the previous year. Net Profit After Tax (NPAT) saw a sharper decline of 40.42%, falling to ₹64.09 crore from ₹107.58 crore in FY 2024-25. The company attributed the profitability challenges to external market dynamics, specifically citing pricing pressure and dumping from global competitors which impacted revenue by approximately 2%.

Reader Takeaway: Revenue and profit declined due to competition; debt-free status and new facility offer future support.

What just happened

NOCIL reported a consolidated revenue of ₹1,302.97 crore and a net profit of ₹64.09 crore for FY26. This represents a decrease from the previous fiscal year's ₹1,392.69 crore revenue and ₹107.58 crore profit. The company has recommended a final dividend of ₹1.50 per share.

Why this matters

For investors, the results highlight a challenging operating environment marked by aggressive global competition and price erosion. Despite the lower profitability, the company's debt-free status and recent facility commissioning are key positives for long-term stability and growth potential.

The backstory

NOCIL is a leading manufacturer of rubber chemicals in India. The company has been focusing on expanding its capacity and diversifying its product portfolio. The recent fiscal year's performance reflects broader industry trends influenced by global supply-demand dynamics and geopolitical factors affecting raw material prices.

What changes now

While the near-term financial performance has been impacted, the company has commissioned its new TDQ facility at Dahej, ahead of schedule and within budget. Further expansion is underway with an integrated specialty rubber chemicals project set to commission in FY 2027-28. These developments are expected to bolster future capacity and offerings.

Risks to watch

Intensified global competition leading to pricing and dumping pressure remains a significant risk. Geopolitical risks, including volatility in crude oil prices and supply chain disruptions, also pose a concern for the industry.

Peer comparison

While specific peer results are not detailed in the filing, the industry broadly faces similar challenges of global competition and raw material price volatility. NOCIL's performance needs to be viewed within this larger context.

Context metrics (time-bound)

Revenue from operations for FY 2025-26 was ₹1,302.97 crore, down 6.44% year-on-year. Net Profit After Tax for FY 2025-26 was ₹64.09 crore, down 40.42% year-on-year. The company achieved a volume growth of 12% in the second half of FY26.

What to track next

Investors should monitor NOCIL's ability to manage pricing pressures, gain market share, and the successful commissioning and ramp-up of its new specialty rubber chemicals project. Progress on volume growth and margin improvement will be key indicators.