South Indian Bank announced its financial results for the fiscal year and fourth quarter ended March 31, 2026. The bank reported a consolidated Net Profit of ₹1,455.64 Cr for the full fiscal year. The net profit for the fourth quarter of FY26 was ₹407.40 Cr.

Key Financial Highlights

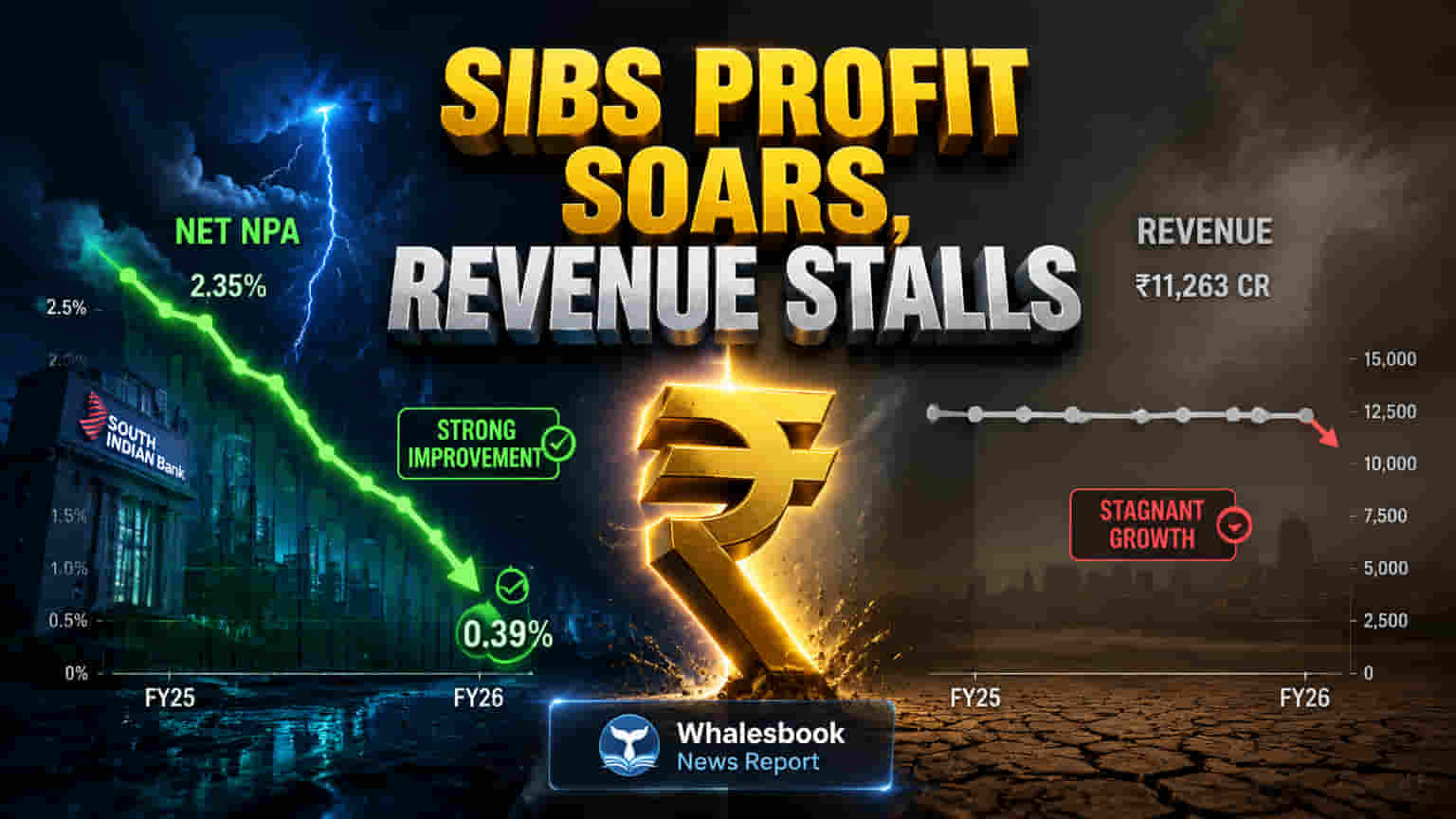

Asset quality showed significant improvement. The bank's Net NPA ratio dropped to 0.29% from 0.92% year-on-year, and Gross NPA declined from 3.20% to 1.43%. Total deposits saw robust growth, increasing from ₹1,07,52,560 lakhs to ₹1,23,34,632 lakhs during the fiscal year. The board recommended a dividend of ₹0.45 per equity share.

What the Numbers Mean

The sharp reduction in non-performing assets (NPAs) significantly lowers the bank's credit risk and potential for future provisioning costs. Strong deposit growth provides a stable, potentially lower-cost funding base for its lending operations. The recommended dividend signals a commitment to shareholder returns.

Strategic Context

South Indian Bank has been strategically focusing on retail and SME penetration and digitization, adopting a 'phygital' approach. The bank completed a rights issue in FY24, significantly strengthening its capital base, with its Capital to Risk-weighted Assets Ratio (CRAR) comfortably near 20%. In the previous fiscal year, FY25, the bank reported a net profit of ₹1,303 Cr, up 22% year-on-year, with Gross NPA at 3.20% and Net NPA at 0.92%. Its total business grew by 11% to ₹1,82,346 crore in FY24.

Performance Implications

Improved asset quality can translate to lower provisioning expenses, bolstering future profitability. Sustained deposit growth will support its lending capacity. The declaration of a dividend provides a direct return to shareholders.

Key Risks to Monitor

Despite asset quality improvements, challenges remain. The bank's quarterly total revenue was nearly flat (-0.01% YoY), and annual revenue growth stood at a modest 5.61%. A significant portion of the bank's portfolio, over two-thirds, is concentrated in Southern India, posing regional risk. In November 2024, the RBI imposed a ₹59.20 lakh penalty for non-compliance with deposit interest and customer service rules. A GST penalty of ₹12.03 lakh was also received in February 2025.

Competitive Landscape

South Indian Bank's FY26 consolidated Net Profit was ₹1,455.64 Cr. Competitors operating in similar segments include Federal Bank, City Union Bank, Dhanlaxmi Bank, and Karur Vysya Bank. Federal Bank focuses on retail, MSME, and corporate banking, while City Union Bank is known for its strong retail and SME presence in South India.

Key Performance Metrics

- Net NPA ratio improved from 0.92% in FY25 to 0.29% in FY26.

- Gross NPA ratio decreased from 3.20% in FY25 to 1.43% in FY26.

- Total deposits grew from ₹1,07,52,560 lakhs in FY25 to ₹1,23,34,632 lakhs in FY26.

- Standalone annual revenue grew by 5.61% in FY26.

- A dividend of ₹0.45 per equity share has been recommended for FY26.

Investor Watchlist

Investors will be watching the management's outlook for FY27 revenue growth drivers. Key areas to track include the sustained improvement in asset quality and its impact on provisioning, trends in Net Interest Margins (NIMs) amidst evolving interest rate scenarios, further diversification of the loan book beyond geographical concentration, and any updates on the GST penalty and regulatory compliance.