SBI Reports Record ₹83,298 Cr Profit for FY26, NPAs Improve

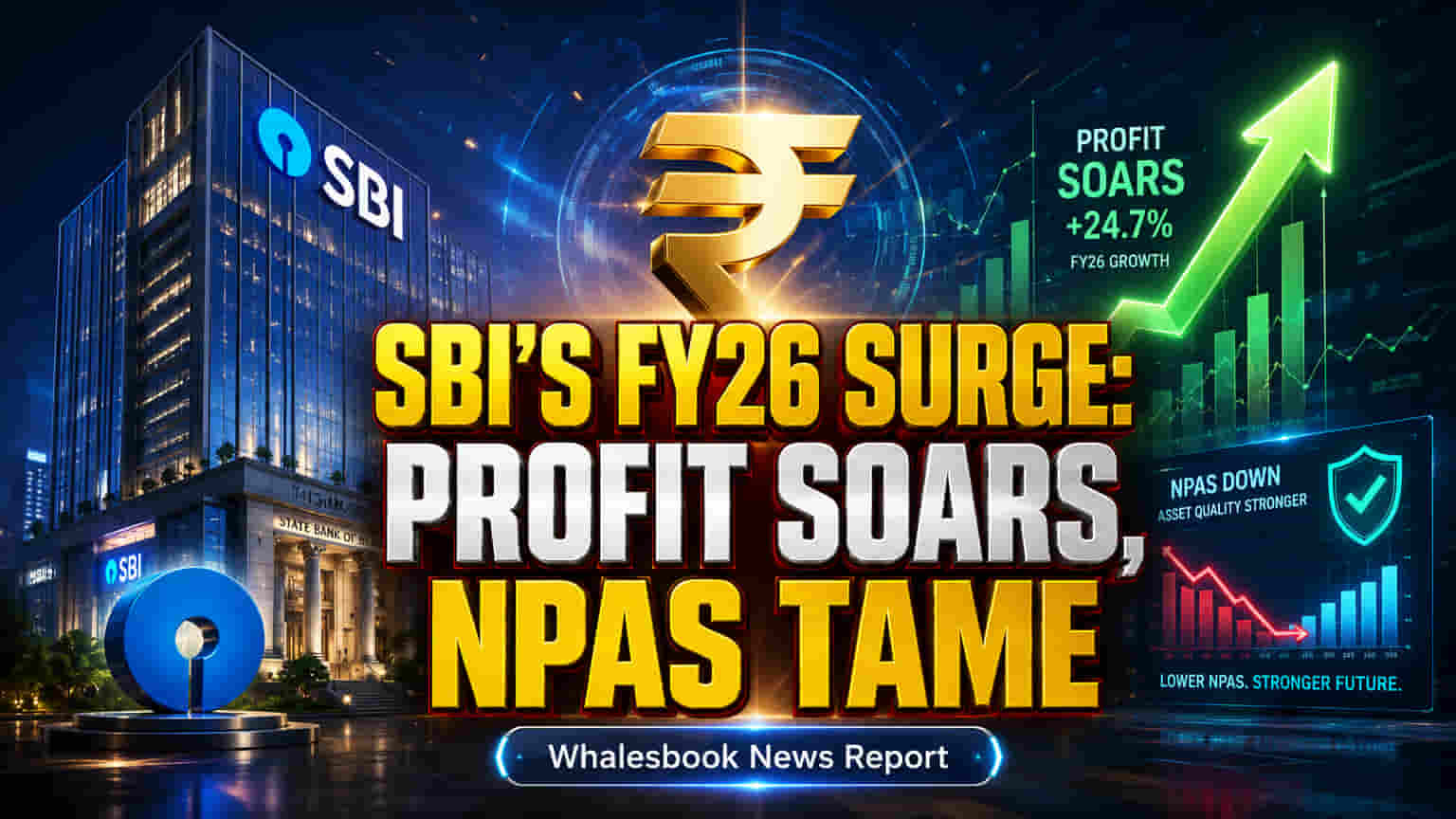

State Bank of India has announced its full-year financial results for FY26, reporting a consolidated net profit of ₹83,298.78 crore. The bank's total consolidated revenue for the fiscal year reached ₹7,09,616.96 crore, an increase of 6.98%.

Quarterly Performance and Asset Quality

For the fourth quarter ending March 31, 2026, SBI posted a consolidated net profit of ₹19,642.87 crore. While annual revenue saw robust growth, the quarterly revenue growth was more modest, rising 0.84% year-on-year. A significant improvement was noted in asset quality, with the standalone Gross Non-Performing Asset (NPA) ratio falling to 1.49% from 1.82% a year earlier.

Shareholder Returns and Exceptional Gains

Shareholders will receive a dividend of ₹17.35 per share. The bank also recorded an exceptional gain of ₹3,026.57 crore from the sale of its stake in Yes Bank. The company's financial statements received a clean audit report.

Financial Strength and Background

These results highlight SBI's strong financial performance and effective operational management. Improved asset quality strengthens the bank's balance sheet, while the Yes Bank stake sale provided a notable boost to profitability. State Bank of India is India's largest public sector bank, offering a wide array of banking and financial services. In recent years, the bank has prioritized enhancing asset quality and expanding its digital banking platforms, contributing to its consistent financial results.

Potential Challenges and Industry Context

The slower quarterly revenue growth of 0.84% bears watching. Potential global and domestic economic slowdowns could also impact future loan demand and asset quality. Regulatory changes might affect banking operations and profitability. SBI's improved Gross NPA ratio of 1.49% places it favorably among public sector peers like PNB and Bank of Baroda, which are also focused on asset quality. Private sector banks like HDFC Bank and ICICI Bank often achieve higher valuations based on their growth and profitability metrics, but SBI's scale and performance remain a benchmark for public sector banks.

What to Watch Next

Investors will be monitoring upcoming quarterly results for sustained revenue growth trends. Management commentary on future strategies and outlook will be key. Further developments in asset quality across the banking sector, the impact of interest rate changes on margins, and the progress of SBI's digital initiatives will also be important factors to track.