Regency Fincorp Reports Significant FY26 Growth

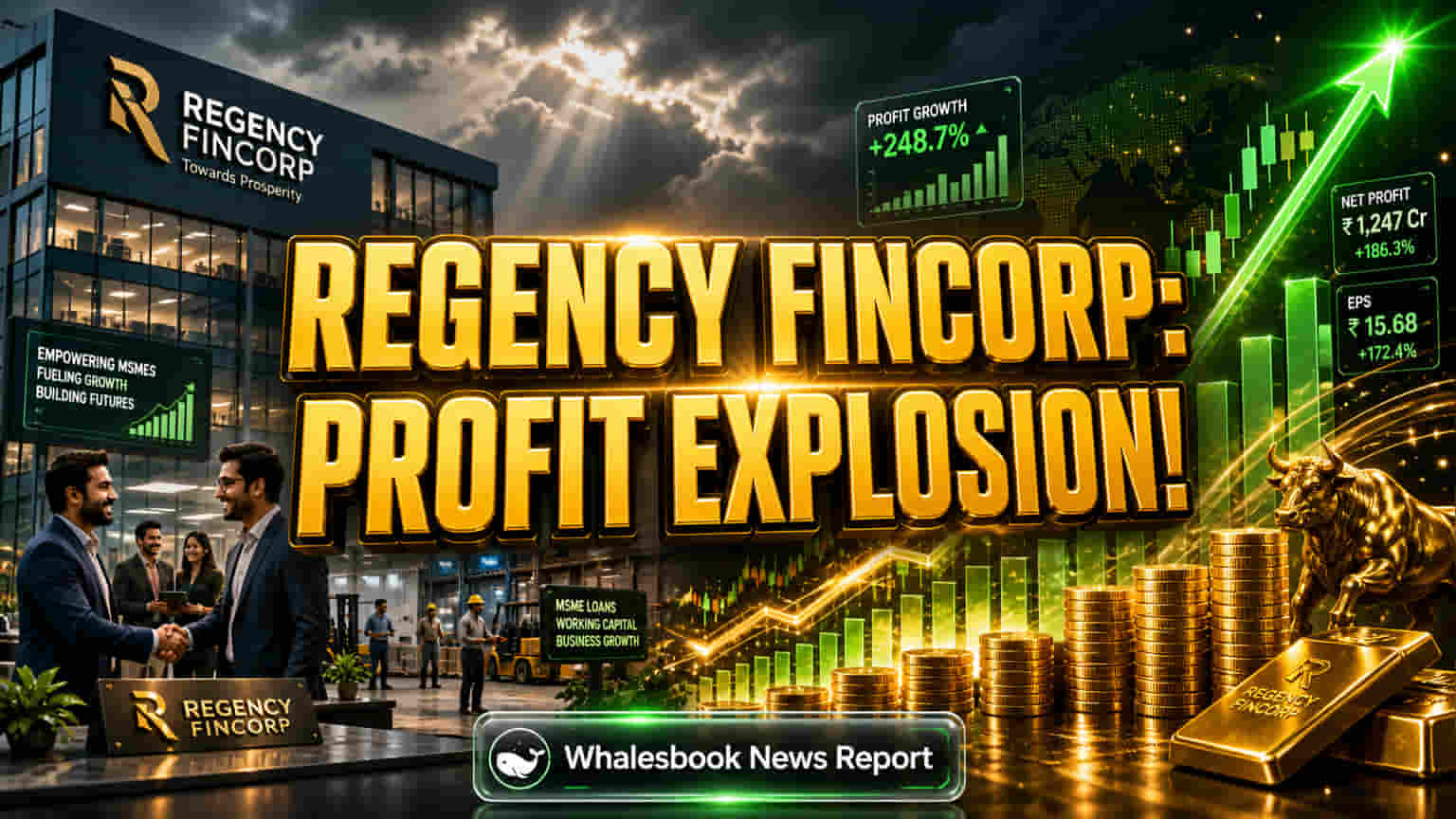

Regency Fincorp Ltd announced exceptional financial results for the fiscal year ending March 31, 2026. The Non-Banking Financial Company (NBFC) achieved a Profit After Tax (PAT) surge of 170% year-on-year, reaching ₹13.40 crore.

Total income for FY26 climbed an impressive 85% to ₹40.10 crore. This strong financial performance was supported by a substantial 45% rise in Asset Under Management (AUM), which grew to ₹261.20 crore.

The company also reported a 43% increase in disbursements, totaling ₹142.10 crore. Key financial metrics showed improvement, with Net Interest Margin (NIM) rising to 10.3%, an increase of 285 basis points. Return on Equity (ROE) also saw a significant jump, reaching 16.7%.

Growth Drivers and Market Position

This robust performance highlights the successful implementation of Regency Fincorp's expansion strategy. Its focus on financing for Micro, Small, and Medium Enterprises (MSME) and retail customers has clearly paid off. The significant growth in income and profit, alongside expanding AUM, points to greater market reach and efficient business operations.

The company's success in raising capital through Non-Convertible Debentures (NCDs) and Compulsorily Convertible Debentures (CCDs) is vital for maintaining its growth pace. This capital access indicates investor trust and provides the funding needed to grow its business further.

Strategic Initiatives and Digital Push

Regency Fincorp has been strategically expanding its lending across MSME and retail sectors, targeting underserved market segments to build a stable business.

The company is also investing in digital tools. Initiatives like CashMySalary and the planned digital wallet 'RegPay' aim to improve customer service and simplify loan processing, positioning Regency Fincorp for the future of digital finance. Capital raised recently, including through NCDs in early 2026, has been key to funding these expansion plans and reinforcing its financial standing.

Implications for Shareholders and Strategy

- Shareholders may see increased value as the company continues its profit growth and market expansion.

- With more capital available, Regency Fincorp is better equipped to fund its ambitious growth plans.

- Digital projects such as RegPay could unlock new income sources and attract different customer groups.

- While focusing on MSME and retail lending can bring higher returns, it also requires close attention to asset quality.

- Tapping into underserved markets presents substantial opportunities for future growth.

Key Risks to Monitor

Although asset quality remains strong overall, Gross Non-Performing Assets (GNPA) edged up by 57 basis points to 0.99%, and Net Non-Performing Assets (NNPA) rose by 43 basis points to 0.74%. These trends need careful watching as the loan book expands.

Relying on debt financing like NCDs means Regency Fincorp must effectively manage interest rate changes and maintain its credit rating.

Peer Landscape

Regency Fincorp operates in the NBFC sector, specifically focusing on MSME and retail lending. This places it alongside other companies targeting growth in these areas. Many competitors are also upgrading digital services and diversifying funding. Firms serving similar customers typically aim for Net Interest Margins (NIMs) between 7-12% and aim to keep Gross Non-Performing Assets (GNPA) below 2-3%.

Future Focus Areas

- How effectively Regency Fincorp executes its plan to raise up to ₹400 crore via NCDs.

- The successful launch and customer uptake of its RegPay digital wallet.

- Ongoing expansion and asset quality in its MSME and retail lending portfolios.

- Any new digital lending projects or collaborations.

- Management's outlook on growth and margin sustainability during future investor calls.