Muthoot Microfin Posts Strong Q4 FY26 Results

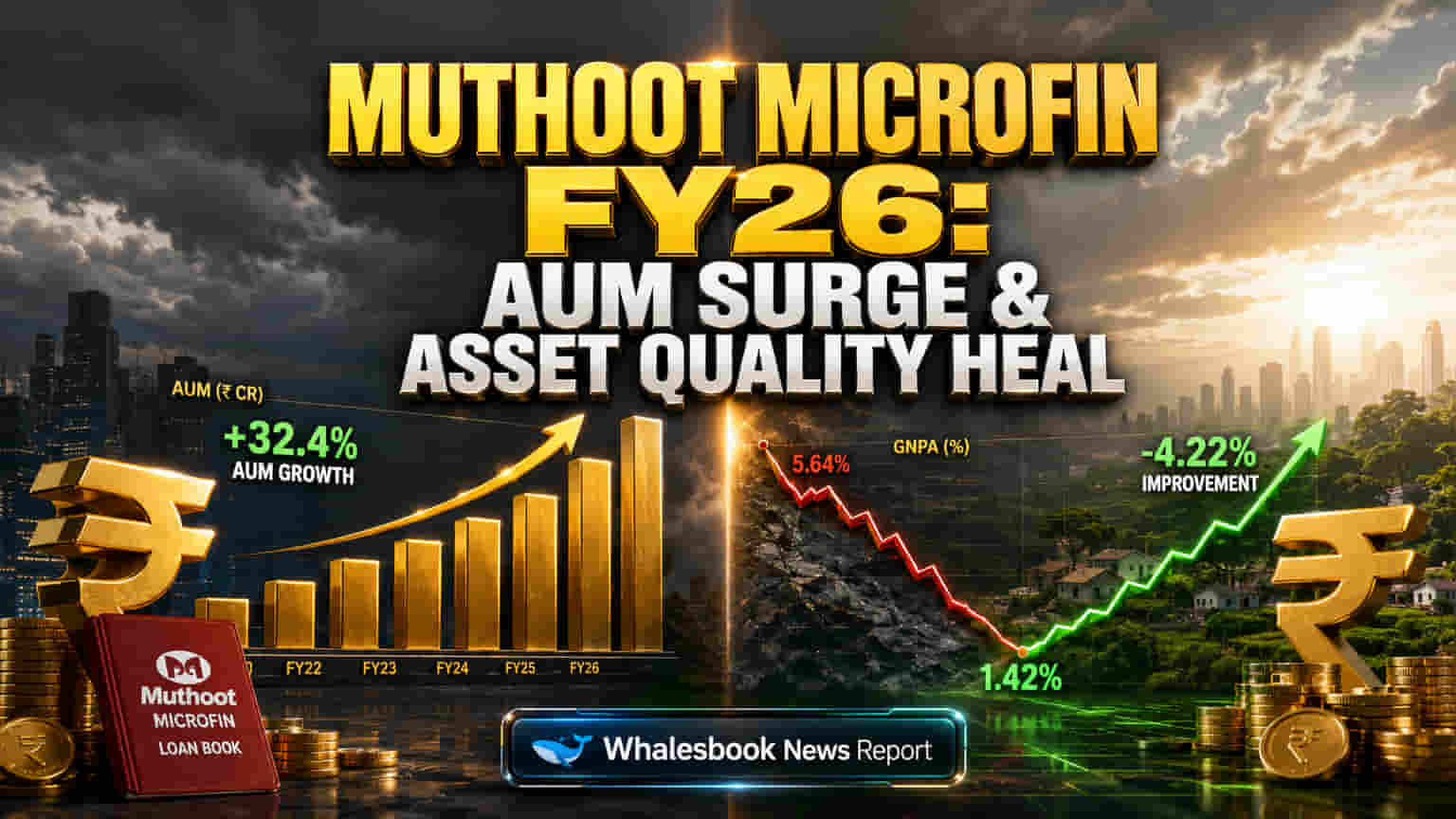

Muthoot Microfin announced its audited financial results for the fiscal year ended March 31, 2026. The company reported a 13.3% year-on-year growth in its Assets Under Management (AUM) to ₹14,005.6 crore.

Key Financials

Asset quality indicators showed improvement. Gross Non-Performing Assets (GNPA) declined to 3.89% in the fourth quarter (Q4) of FY26, down from 4.84% in the same period last year. Net NPA also improved to 1.14%.

For Q4 FY26, the company posted a Profit After Tax (PAT) of ₹71.1 crore. The Pre-Provisioning Operating Profit (PPOP), a measure of core operational profitability, grew significantly by 48.0% year-on-year to ₹192.8 crore.

Additionally, Mr. Akshaya Prasad resigned as a Non-Executive Director, effective May 6, 2026.

What the Numbers Mean

These results indicate a notable recovery for Muthoot Microfin following challenges in FY25. The growth in AUM, coupled with improved asset quality metrics like lower GNPA and strong collection efficiency (96.43% for FY26), points to strengthening business momentum.

The substantial rise in PPOP suggests better operational efficiency and cost management. This was achieved even as the Cost of Funds for FY26 declined by 75 basis points to 10.27%.

Past Challenges and Strategy

Fiscal Year 2025 saw sector-wide challenges in microfinance, leading to increased provisions and a net loss for Muthoot Microfin in Q4 FY25. In Q2 FY26, the company reported a profit fall and rising GNPA, indicating ongoing difficulties.

To address this, Muthoot Microfin has been strategically diversifying its loan portfolio, expanding into individual loans, micro-LAP, and gold loans. This has increased its non-Joint Liability Group (JLG) product mix to 17%.

Recently, SEBI granted promoter family trusts an exemption from open offer obligations following an internal restructuring aimed at streamlining succession planning.

Implications for the Future

Shareholders can anticipate a more stable growth trajectory supported by improved AUM and better asset quality. The company's focus on operational efficiency, reflected in PPOP growth, could lead to enhanced profitability in the medium term.

The resignation of a non-executive director will require a review of board composition and governance oversight.

Diversification efforts may contribute to a more resilient and less volatile business model.

Potential Risks

The microfinance sector can be affected by regulatory changes and local economic disruptions. The resignation of Mr. Akshaya Prasad could lead to scrutiny on board dynamics and succession planning. While improving, GNPA at 3.89% still indicates a level of credit risk.

Peer Comparison

Muthoot Microfin's peers, such as Bandhan Bank and Equitas Small Finance Bank, also reported strong Q4 FY26 results. Bandhan Bank saw a 68% YoY profit jump to ₹530 crore with improving GNPA, while Equitas SFB posted a 406% YoY PAT surge to ₹213 crore, driven by margin growth. Ujjivan SFB reported a 23.24% YoY decline in PAT to ₹83.37 crore.

Muthoot's PAT of ₹71.1 crore is lower than these peers, but its AUM growth and PPOP jump are positive signals.

Looking Ahead

Investors will be monitoring:

- The continued trajectory of AUM growth and its sustainability.

- Asset quality metrics, particularly GNPA and collection efficiency.

- The impact of the director's resignation on board governance and future strategic decisions.

- The performance of diversified loan products and their contribution to overall profitability.

- The evolving regulatory landscape for NBFC-MFIs.