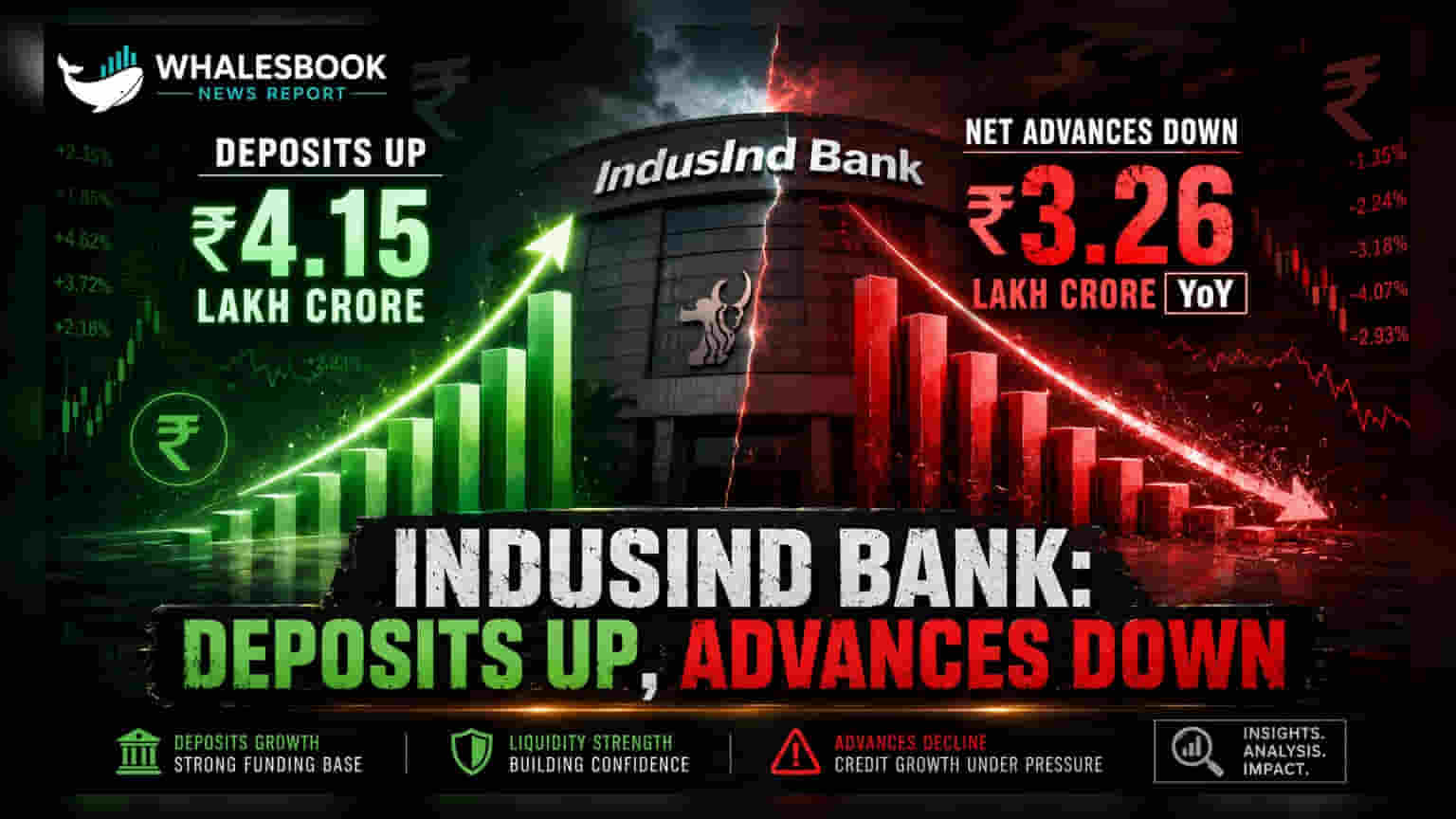

IndusInd Bank reported provisional Q1 FY27 results showing a 4.5% rise in deposits to ₹4,14,992 crore. However, net advances fell 2.3% year-on-year to ₹3,26,171 crore, with CASA ratio declining to 29.5%.

IndusInd Bank Q1 FY27 Provisional Financial Highlights

**Deposits:** ₹4,14,992 crore (up 4.5% YoY, 3.8% QoQ) **Net Advances:** ₹3,26,171 crore (down 2.3% YoY, up 3.3% QoQ) Reader Takeaway: Strong deposit growth is positive, but falling advances and CASA ratio need monitoring. ## What just happened IndusInd Bank released its provisional financial results for the quarter ended June 30, 2026 (Q1 FY27). The bank reported a healthy growth in its total deposits, reaching ₹4,14,992 crore, an increase of 4.5% compared to the previous year and 3.8% sequentially. However, its net advances saw a 2.3% year-on-year decrease, although they increased by 3.3% quarter-on-quarter, standing at ₹3,26,171 crore. ## Why this matters The divergence between deposit and advance growth, coupled with a declining CASA ratio, are key indicators for the bank's profitability. A falling CASA ratio (down to 29.5% from 31.5% last year) can lead to higher funding costs and potentially pressure the Net Interest Margin (NIM). ## The backstory IndusInd Bank has been focusing on growing its retail and small business deposits, which reached ₹1,93,618 crore as of June 30, 2026. This segment showed growth both sequentially and year-on-year, indicating a strategy to build a stable funding base. ## What changes now Investors will be watching how the bank manages its funding costs amidst the CASA ratio compression and whether the recent sequential growth in advances can sustain and reverse the year-on-year decline. The provisional figures are subject to a limited review by statutory auditors. ## Risks to watch The primary risks highlighted are the compression in the CASA ratio, which could impact NIM, and the year-on-year contraction in net advances, signalling a slowdown in credit offtake compared to the prior year. ## Peer comparison While specific peer data for Q1 FY27 is not yet available, a declining CASA ratio and moderating advance growth are trends that investors will compare across other private sector banks as their results are released. ## Context metrics (time-bound) - **Total Deposits:** ₹4,14,992 crore (June 30, 2026) vs ₹3,97,144 crore (June 30, 2025) - **Net Advances:** ₹3,26,171 crore (June 30, 2026) vs ₹3,33,694 crore (June 30, 2025) - **CASA Ratio:** 29.5% (June 30, 2026) vs 31.5% (June 30, 2025) ## What to track next Investors should monitor the bank's Net Interest Margin (NIM) in the upcoming quarterly results, the sustained growth in net advances, and any commentary on strategies to improve or stabilize the CASA ratio.