Q4 FY26 Financial Highlights

IDFC First Bank reported a substantial 145.3% year-on-year surge in Normalized Profit After Tax (NPAT) for the fourth quarter of fiscal year 2026, reaching ₹746 crore. This adjusted figure provides a deeper insight into the bank's operational performance compared to the reported Profit After Tax (PAT) of ₹319 crore, which grew 4.9% year-on-year. For the full fiscal year FY26, reported PAT was ₹1,636 crore, up 7.3% from the previous year. Net Interest Income (NII) also showed strong growth, increasing by 15.7% year-on-year to ₹5,677 crore for the quarter.

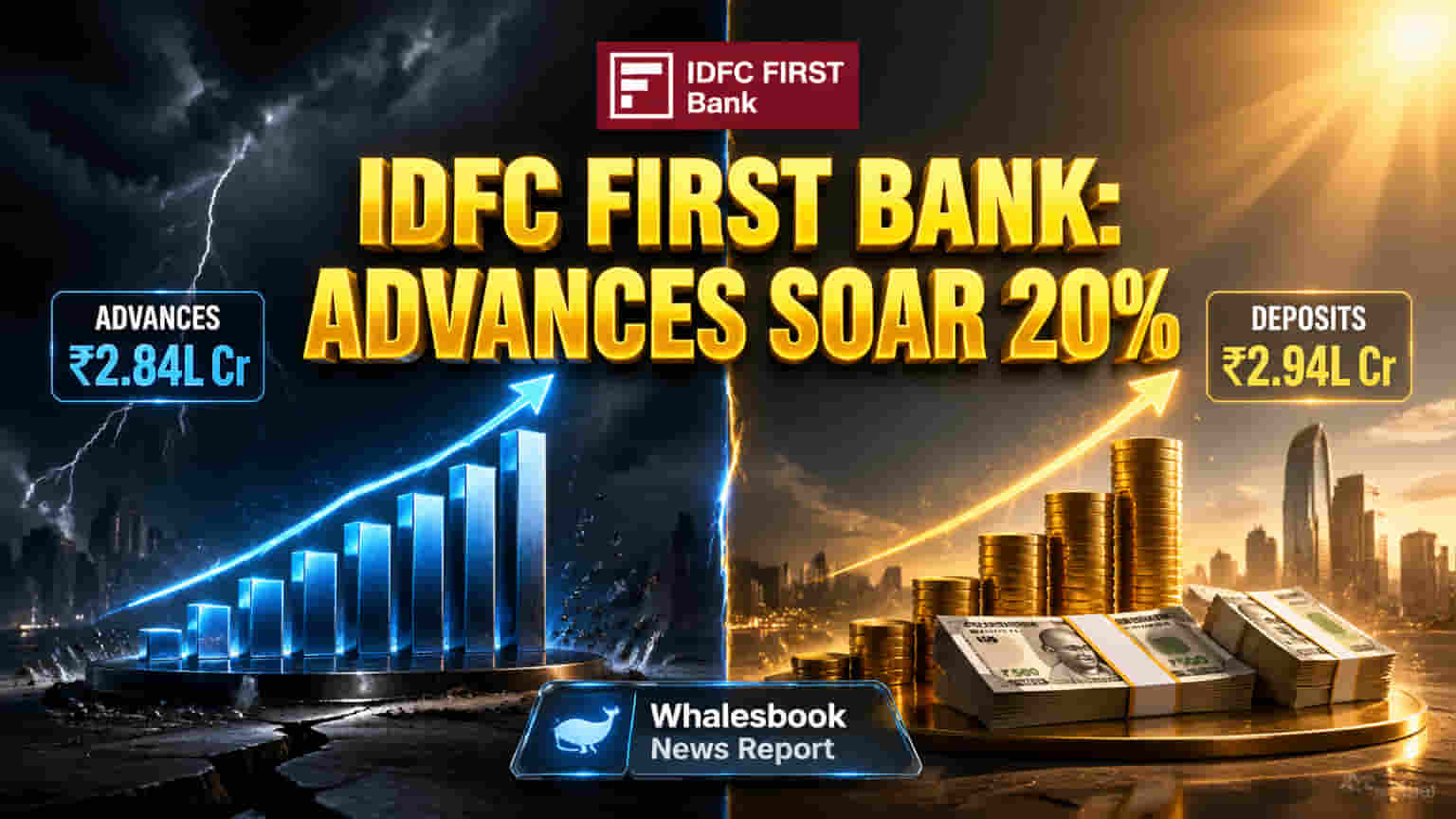

Key Growth Drivers

The bank's aggressive business expansion is evident in its Gross Advances, which climbed 20% year-on-year to ₹2.84 lakh crore. This lending growth was supported by a solid 17% rise in Total Deposits, which reached ₹2.94 lakh crore. This indicates increasing market penetration and strong customer acquisition. Asset quality remained a strong point, with the Gross Non-Performing Asset (GNPA) ratio at 1.61% and the Net Non-Performing Asset (NNPA) ratio at 0.48% as of March 2026.

Strategic Context

IDFC First Bank continues to execute its strategy focused on retail and MSME lending to build a robust balance sheet. This focus comes after facing challenges in FY25, which saw a decline in net profit due to higher provisions and microfinance stress. Despite those headwinds, FY25 advances grew by 19.8%, and customer deposits increased by 25.5% by June 30, 2025. The bank previously outlined plans to double its balance sheet within four years, supported by a ₹7,500 crore capital infusion.

Investor Outlook

Shareholders can observe the bank's increasing scale of operations driven by its expanding retail and MSME loan book. The sustained focus on deposit growth suggests a stable funding base for future expansion. The significant jump in normalized PAT points towards improving operational efficiency and enhanced profitability.

Potential Risks

The bank has faced regulatory scrutiny, including penalties from the Reserve Bank of India (RBI). These include a ₹1 crore fine in April 2024 for loan advance restrictions and ₹38.60 lakh in April 2025 for KYC lapses. IDFC First Bank also identifies potential risks such as significant changes in financial regulations, challenges in meeting capital adequacy requirements, and issues related to collateral valuation or NPA management. Operational risks, including fraud and cybersecurity incidents, remain constant watchpoints.

Competitive Landscape

IDFC First Bank's 20% retail loan growth reflects an assertive market strategy. While established giants like HDFC Bank and ICICI Bank lead the market, IDFC First Bank is carving out its specific niche through strong retail expansion. Competitors such as State Bank of India and Axis Bank also operate in this space with their own distinct strategies and market positions.

Key Financial Metrics

- Net Interest Margin (Standalone): 5.93% for Q4 FY26.

- Gross Non-Performing Asset Ratio (Standalone): 1.61% as of March 2026.

- Net Non-Performing Asset Ratio (Standalone): 0.48% as of March 2026.

Key Areas to Monitor

Investors will be watching the sustainability of the bank's 20% loan growth alongside its deposit growth. Monitoring Net Interest Margin (NIM) trends and the impact of the funding mix will be crucial. The bank's management of its microfinance portfolio and its effect on asset quality and provisions will also be closely observed. Efforts to improve credit costs, capital adequacy ratios, and operational leverage as the business scales will be key indicators.