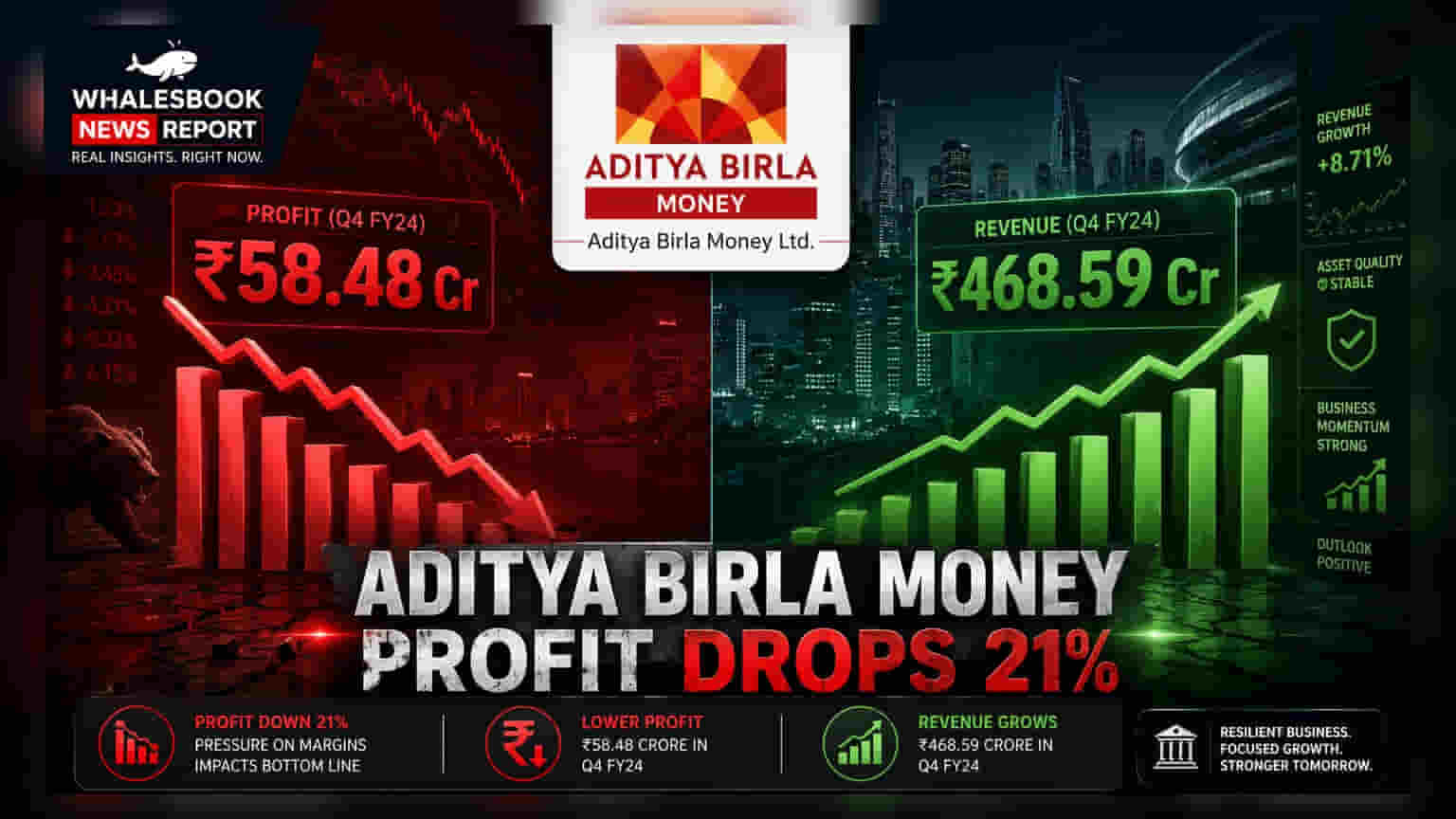

Aditya Birla Money reported a 21.18% drop in profit after tax to ₹58.48 crore for FY26, despite a 3.41% rise in revenue from operations to ₹468.59 crore. The company did not recommend any dividend.

Aditya Birla Money Sees Profit Dip Amidst Revenue Growth in FY26

Aditya Birla Money's Profit After Tax fell 21.18% to ₹58.48 crore in FY26 from ₹74.19 crore in FY25. Revenue from operations grew 3.41% to ₹468.59 crore.

Reader Takeaway: Strong revenue growth and digital migration contrasted by a significant profit decline and no dividend.

What just happened

Aditya Birla Money Ltd announced its financial results for the fiscal year ending March 31, 2026. The company reported a revenue from operations of ₹468.59 crore, an increase of 3.41% compared to ₹453.15 crore in the previous fiscal year. However, its profit after tax (PAT) saw a substantial decline of 21.18%, falling to ₹58.48 crore from ₹74.19 crore in FY25. The operating profit margin also decreased to 17% from 22% in the prior year.

Why this matters

The dip in profitability despite revenue growth and moderating margins signals potential pressure on the company's earnings efficiency. The decision not to recommend a dividend for FY26 indicates a focus on conserving cash, possibly for future investments or to manage working capital needs. The proposed increase in authorised capital suggests a strategic move for future expansion or funding requirements.

The backstory

In FY25, Aditya Birla Money had reported a profit of ₹74.19 crore on revenues of ₹453.15 crore, with a higher operating profit margin of 22%. The company has been focused on digital transformation, successfully migrating all users to its new ELEVATE ecosystem. Its Margin Trading Facility (MTF) book has shown significant growth, crossing the ₹1,000 crore mark.

What changes now

With the reduced profitability and no dividend payout, investors may need to re-evaluate their expectations for short-term returns. The proposed increase in authorised share capital from ₹33 crore to ₹333 crore, pending member approval, indicates a strategic intent for future capital infusion or business expansion.

Risks to watch

Key concerns include the significant year-on-year decline in PAT and the moderation in operating profit margins. A penalty of ₹2.13 lakh imposed by the NSE for client code modifications also presents a compliance-related risk.

Peer comparison

While specific peer financial data for FY26 is not immediately available in the filing, the brokerage segment saw a 4% decline in revenue, while the wholesale debt market segment grew by 38%. This indicates a shift in revenue contribution within the company's own segments.

Context metrics (time-bound)

- Revenue from operations: ₹468.59 crore (FY26) vs ₹453.15 crore (FY25) - up 3.41%

- Profit After Tax: ₹58.48 crore (FY26) vs ₹74.19 crore (FY25) - down 21.18%

- Operating Profit Margin: 17% (FY26) vs 22% (FY25)

- Margin Trading Facility (MTF) book crossed ₹1,000 crore during FY26.

What to track next

Investors will be watching the company's performance in the upcoming financial year (FY27), particularly its ability to improve profitability and operating margins. The progress on the proposed increase in authorised share capital and its utilization will also be a key area to monitor.