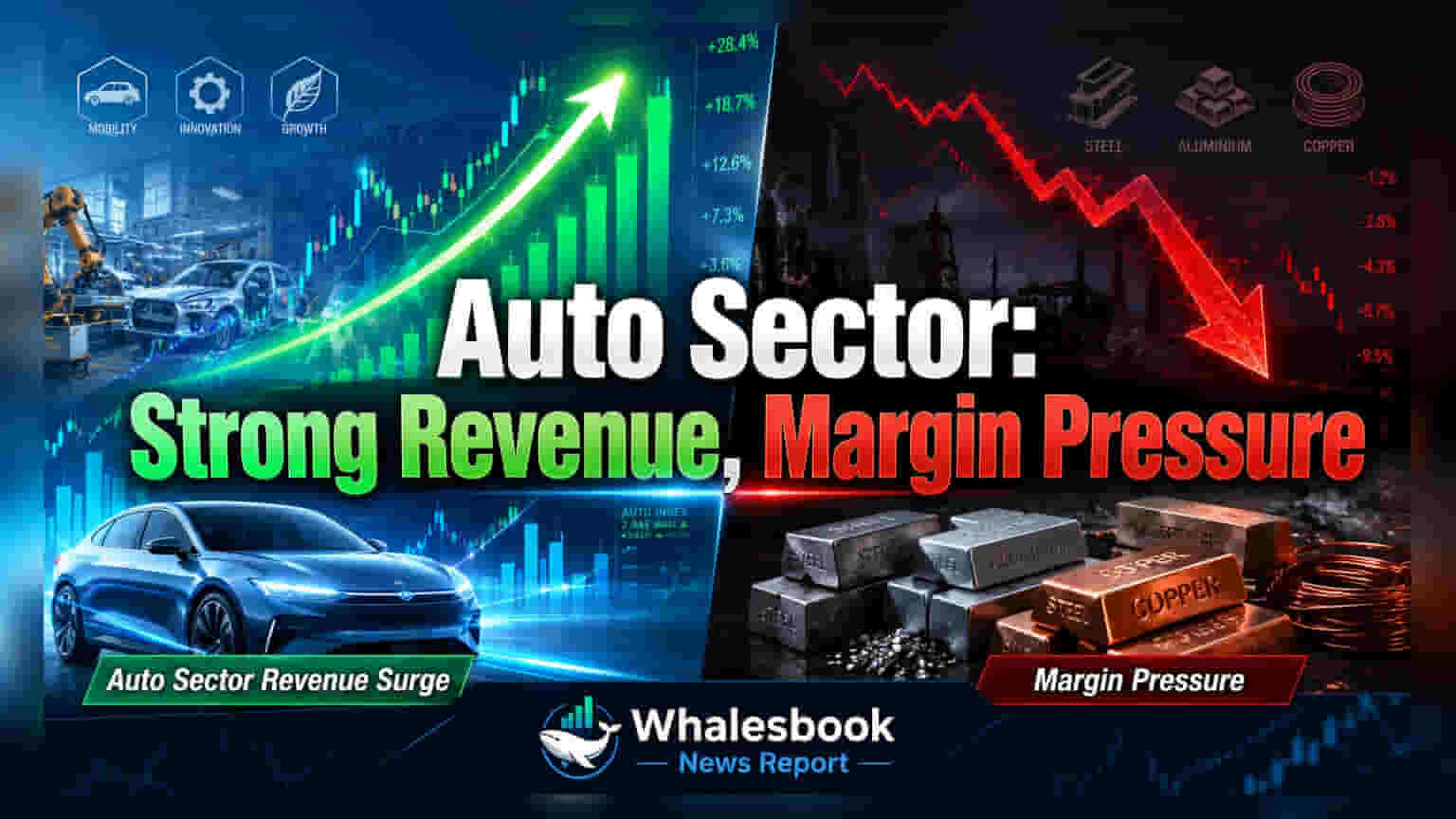

A research report indicates robust revenue growth for auto OEMs and ancillaries, driven by demand and premiumization. However, rising commodity prices are expected to pressure near-term profitability despite price hikes.

Auto Sector Poised for Strong Q1FY27 Revenue Growth Amid Margin Pressures

Expected YoY Growth: Revenue ~31% (Auto OEMs), ~18.4% (Auto Ancillaries); EBITDA ~35% (Auto OEMs), ~17.6% (Auto Ancillaries).

Reader Takeaway: Resilient demand drives revenue, but rising commodity costs challenge near-term profit margins.

What Just Happened

A recent research report forecasts significant year-on-year revenue growth for the Indian auto sector in Q1FY27. Auto Original Equipment Manufacturers (OEMs) are expected to see revenue rise by approximately 31%, with EBITDA growing around 35%. Auto ancillary companies are also projected to post strong results, with revenue up by an estimated 18.4% and EBITDA by 17.6%.

Why This Matters

The report highlights a positive demand environment for automobiles, fueled by increasing volumes, a trend towards premium vehicles, and better consumer affordability. While earnings are expected to grow, driven by higher sales volumes, profitability faces near-term challenges. Companies have implemented price increases, but the full impact on margins is anticipated to take time.

The Backstory

The automotive industry has been navigating a complex landscape. Strong domestic demand, especially for passenger vehicles, has been a key growth driver. However, volatile raw material prices, including steel, aluminium, and copper, have consistently posed a challenge to manufacturers' profitability. Geopolitical issues also add to supply chain uncertainties.

What Changes Now

Companies are expected to focus on managing input cost volatility through operational efficiencies and product mix optimization. While price hikes offer some relief, the lag in their benefit means margins could remain under pressure in the immediate quarter. Investors are advised to watch for management commentary on pricing power and margin recovery.

Risks to Watch

- Input Cost Inflation: Significant increases in steel (11% QoQ), aluminium (10% QoQ), and copper (4% QoQ) directly impact the cost of goods sold.

- Supply Chain Risks: Geopolitical tensions, especially concerning Middle East supply chains, could disrupt oil and gas availability, affecting production.

- Margin Lag: The full benefit of recent price increases on company profits will take time to materialize.

Peer Comparison

Key players like Maruti Suzuki are expected to see robust revenue (36.9%) and EBITDA (41.9%) growth, supported by product mix. TVS Motors (Revenue 32.1%, EBITDA 34.9%) and Bajaj Auto (Revenue 33.1%, EBITDA 38.6%) are also poised for strong growth, with exports aiding Bajaj's margins. Escorts Kubota faces margin pressure from raw materials, despite a 26.9% revenue growth expectation. Ashok Leyland anticipates margin improvement alongside a 11.9% revenue and 26.0% EBITDA growth.

Context Metrics (Time-Bound)

Input commodity price changes (QoQ):

- Steel HRC Price: +11%

- LME Aluminium Price: +10%

- LME Copper Price: +4%

What to Track Next

Investors should closely monitor upcoming quarterly results for detailed financial performance, particularly the impact of commodity costs and the effectiveness of pricing strategies on profit margins.